The new ways of consuming information and the related products have experienced an incredible turnaround through the impact of the mobile era: smartphones and smart watches and tablets have transformed the way in which users, who are also customers, relate to the offering surrounding them. This has entailed a significant impact on the banking business: products are being transformed, consumer habits are changing, business is evolving. And no bank can escape that mutation.

The mobile era is the reforming seed with two key elements: the future of banks lies in their evolution to a Platform as a Service (PaaS), based on a strong commitment to application development interfaces for designing products adapted to new consumption and the opening of a new business space in their relationship with third-party suppliers; and secondly, the arrival of the European PSD2 legislation (Revised Directive on Payment Services), amending the entire financial scenario in the EU because it forces banks to provide mandatory access to data and payment services to other companies.

Who are these other companies? Companies that are known as fintechs and concentrate their business in two key sectors: payment initiation services (PIS) and account information services (AIS). In both cases, two businesses that base their consumption habits on digital processes, apps and the use of smart mobile devices.

Details of the new banking environment

Today most people have a smartphone or another mobile device where they can download banking and financial apps to consult account transactions and cards, make transfers and savings plans, request information on complex financial products, etc. There are reports that analze this new environment for the banking business:

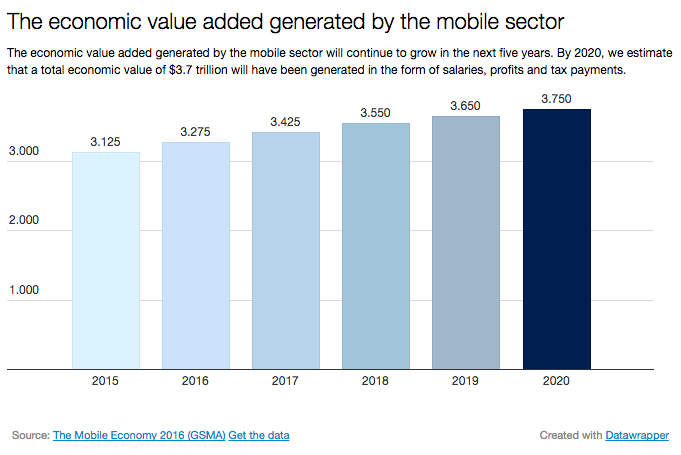

● The value of the economy linked to sectors with mobile products and services will continue to grow in the coming years. The study ‘The Mobile Economy 2016’ by GSMA makes a forecast until 2020. It is clear that there is a fairly juicy pie for companies that decrypt the keys generating revenue through mobile devices. Banks are another player in this area. Here is a chart with the economic trend:

● The report ‘Consumers and Mobile Financial Services 2016’ is a fairly recent in-depth study of what the mobile market is like in the US. Some of the figures are revealing: 87% of Americans have a cell phone, data similar to 2014 and 2013; 77% of those cell phones are smartphones, up from 71% in 2014 and 61% in 2013.

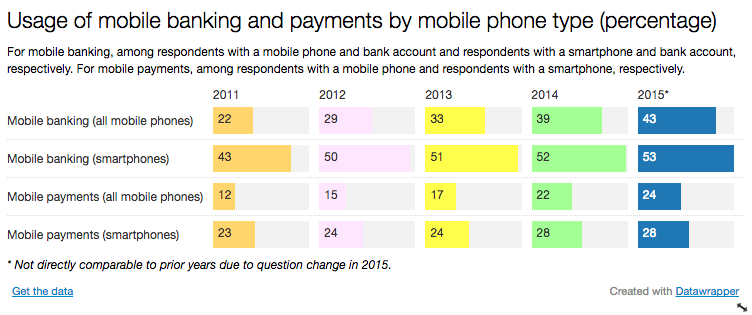

● The same analysis provides some figures on the adoption of financial services in the mobile age: 43% of Americans had used a bank account through their phone in the previous 12 months, compared with 39% in 2014 and 33% in 2013; that data rises to 53% in smartphones compared to 52% in 2014; 28% of smartphone users made use of mobile payments, especially to pay bills, purchase digital content and finally purchase a product in an e-commerce store . This chart summarizes the trend in all these figures between 2011 and 2015:

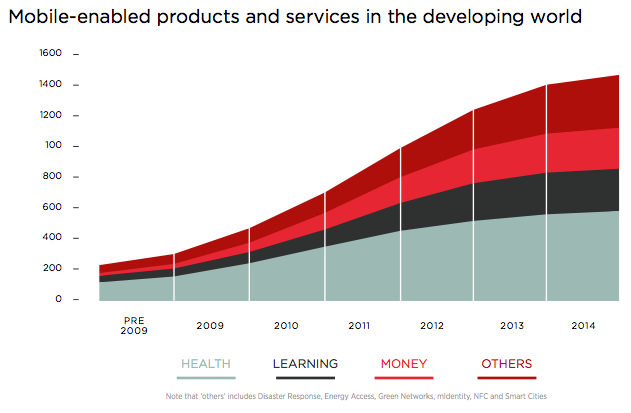

● The report ‘The Mobile Economy 2015’ by GSMA provides some interesting data and forecasts about new mobile business for international banking. Credit services through a mobile wallet, which have been expanded thanks to agreements between operators and banks; mobile insurance, which is in decline; and financial services related to mobile devices, on the rise thanks to the new mobile era . It is certainly true that nowadays there are more mobile products and services related to the health sector, but the financial ones are very much on the rise. .

Access to banking services in the mobile era

Mobile banking and mobile payments are being taken up rapidly among the population for many reasons: the burden of physical products such as cards, coins or banknotes is removed; it is a fairly flexible method linked to any bank account, online payment systems like PayPal or cryptocurrencies such as Bitcoin; and also a more agile way thanks to the use of communication technologies and payments such as NFC (Near Field Communication).

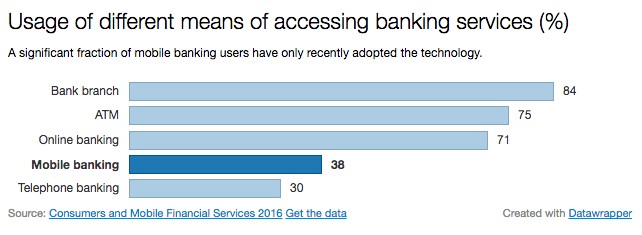

However, customers still prefer other methods of relationship with banks, whether it be a branch, an ATM or online banking, to the detriment of other options such as mobile banking or telephone banking.

Mobile banking users tend to use their smartphones to make all kinds of financial arrangements from their devices: more than 80% have downloaded their bank’s app to make transactions (balance inquiries, transfers between their own accounts or accounts of other users, receiving banking information through or email notifications, etc.) In some cases, customers have also made use of a technology known as remote deposit capture: using the phone’s camera to take a picture of the amount of a check to pay in and make the deposit.

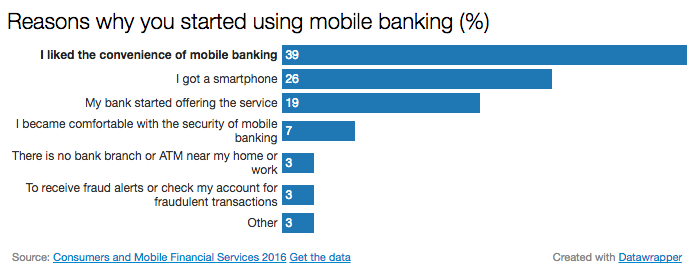

Normally, when you ask a mobile banking user the reasons why they use these services, or the same is done with other users who prefer other types of access to financial services, the answer always revolves around three important concepts: ease, speed and flexibility. The reasons given are always related to how the bank made those services available, there are no branches or ATMs near their home or work or they believe that mobile banking offers secure services and the ease to check possible fraud.

Mobile payments and security

The implementation of mobile payments is taking place progressively throughout the world. Bill payments, purchasing physical goods or payment of subscriptions of any kind of content (media or services like Netflix) are the most common uses by users, but the habit of buying at mobile sale points (MPOS) is increasing in customers with a smartphone, they are associated with a personal account, a debit card, a credit card or a PayPal-type account.

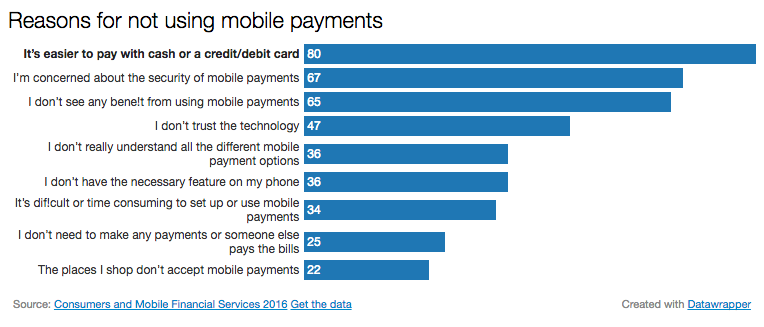

There are commercial banking customers who do not make use of mobile payments yet for several reasons: some believe it is easier to pay with cash or use a card, while others still do not trust the security of the method, they do not see real use or understand the different types of mobile payments.

If you want to find out more about BBVA’s financial APIs, go to this website.

If you want to try BBVA’s APIs, test them here.